Accounting information is expected to possess certain qualitative characteristics to ensure its usefulness and reliability for decision-making purposes. In this article, you can see the top 10 Qualitative Characteristics of Accounting Information that are very useful in the smooth working of accounting information. These characteristics increase the quality of the data. These qualitative characteristics, as defined by the International Financial Reporting Standards (IFRS), include:

Major Qualitative Characteristics of Accounting Information

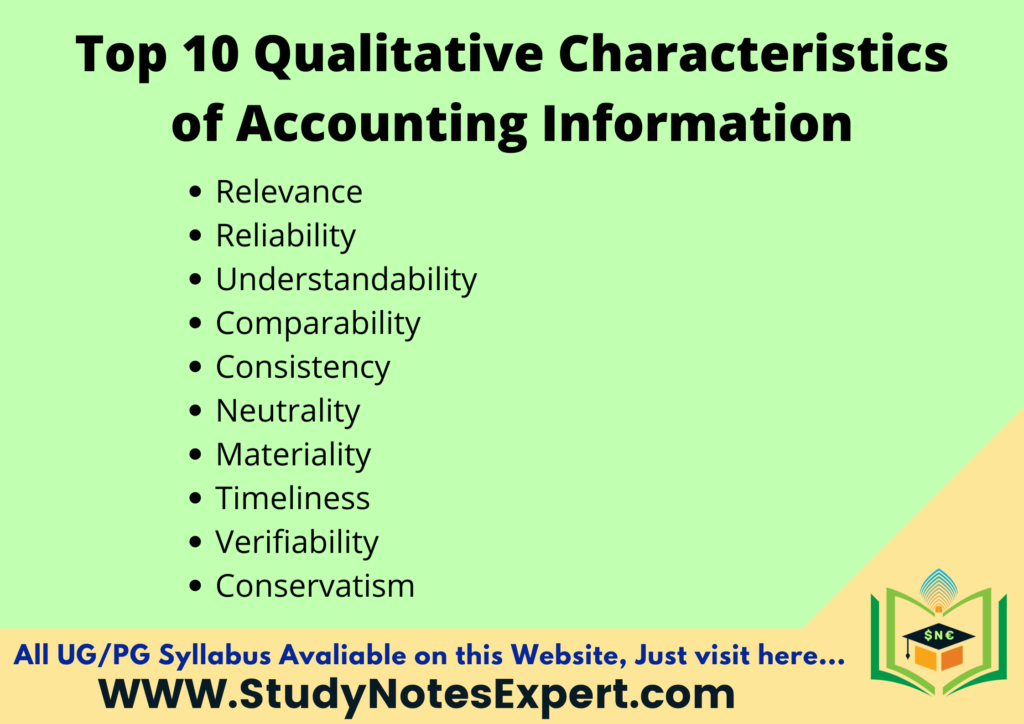

1. Relevance

Relevance is the most important qualitative characteristics of accounting information. It is closely and directly associated with the concept of practical information relevance. It implies that each of those data items should be reported, which will aid the users in making decisions and predictions. In general, the information given greater weight in decision-making is more relevant. Especially its information’s capacity to form a difference that identifies it as appropriate to a choice.

2. Reliability

Reliability is the primary quality that makes accounting information useful for decision-making. Reliable information is required to judge a firm’s earning potential and financial position. Reliability differs from item to item. Some data items presented in an annual report could also be more reliable than others, which is an essential part of qualitative characteristics of accounting information.

3. Understandability

Understandability is the quality of data that permits users to perceive its significance. The benefits of data could also be increased by making it more understandable and useful to a wider circle of users. Presenting information that can be understood only by sophisticated users. It does not create a bias inconsistent with the standard of adequate disclosure. Presentation of data shouldn’t only facilitate understanding and avoid wrong interpretation of monetary statements.

Also Read: Accounting as an Information System

4. Comparability

The economic decision requires choosing among possible courses of action. In making decisions, the decision-maker will compare alternatives facilitated by financial information. Comparability implies possessing things reported during an identical fashion and in contrast to items reported differently. Comparable financial accounting information presents similarities and differences within the enterprise or enterprises and their transactions, not merely from differences in financial accounting treatment.

5. Consistency

Consistency of method throughout your time may be a valuable quality that creates accounting numbers more useful. Consistent use of accounting principles from one accounting period to another enhances the utility of monetary statements. Its users by facilitating analysis and understanding of comparative data.

6. Neutrality

Neutrality is additionally referred to as the standard of ‘freedom from bias’ or objectivity. In formulating or implementing measures, neutrality means that the first concern should be relevance. It is also reliable of the knowledge that results not the effect that the new rule may wear to a specific interest or user.

7. Materiality

The concept of materiality permeates the whole field of accounting and auditing. The materiality concept implies that not all financial information needs or should be communicated in accounting reports-only material information should be reported. Immaterial information may and doubtless should be omitted. The qualitative characteristics of accounting information should be disclosed within the annual report. It probably influences the users’ economic decisions. Information that meets this requirement is material.

8. Timeliness

Timeliness means having information available to decision-makers before it loses its capacity to influence decisions. Timeliness is an ancillary aspect of relevance. If information is either not known when it is needed or becomes available long after the reported events that it’s no value for future action, lacks relevance, and is of little or no use. The timeliness alone cannot make information relevant. Still, a scarcity of timeliness can rob information of relevance it’d otherwise have had.

9. Verifiability

The quality of verifiability contributes to the usefulness of accounting information. It plays a main role in the qualitative characteristics of accounting information. Because verification aims to supply a big degree of assurance that accounting measures represent what they purport to portray. The Validation doesn’t guarantee the suitability of the method used, much less the correctness of the resulting estimate. It does convey some assurance that the measurement rule used whatever it had been was applied carefully and without personal bias on the part of the measurer.

10. Conservatism

There is a neighborhood for a convention like conservatism meaning prudence in financial accounting and reporting. Business and economic activities are surrounded by uncertainty, but they must be applied with care. Conservatism in financial reporting shouldn’t connote deliberate, consistent understatement of net assets and profits. Conservatism may be a prudent reaction to uncertainty to make sure that uncertainties and risks inherent in business situations are adequately considered.

Conclusion

Here we have discussed the qualitative characteristics of accounting information that are very crucial. These qualitative characteristics collectively aim to provide users with reliable and relevant information that assists in understanding the financial position, performance, and changes in financial position of an entity, thus facilitating effective decision-making.

What are the Main Qualitative Characteristics of Accounting Information?

The main qualitative characteristics of accounting information are

1. Relevance 2. Reliability 3. Comparability 4. Understandability 5. Conservatism 6. Timeliness 6. Verifiability.

What are the Main Characteristics of Accounting?

The main characteristics of financial accounting are:

1. Accounting is a process of recording, classifying, and summarizing financial transactions to provide information that is useful in making business decisions.

2. Accounting is governed by generally accepted accounting principles (GAAP), which provide guidance for financial reporting.

3. Accounting information is used by investors, creditors, and other interested parties to make decisions about whether to invest in, lend to, or do business with a company.

4. Accounting data is used to prepare financial statements, which show a company’s financial position, performance, and cash flow.

5. Financial statements are used to make decisions about how to allocate resources and manage risk.

Also Read: Information, Functions, Advantages and Limitations of Accounting

In this article, we have explained the all top qualitative characteristics of Accounting Information. This topic writes for colleges and University exams.