Managerial decision making follows a different process than personal decision-making as it requires more focus on systematic and specialized operations. Decision-making is a complex process. The main obstacles in the process of decision making in marginal costing are inadequate information, conflicting motives, and changing circumstances. A solid decision-making process is integral to good management as it helps in optimum allocation of resources and accomplishment of objectives. Marginal costing techniques may be used for making the following managerial decisions:

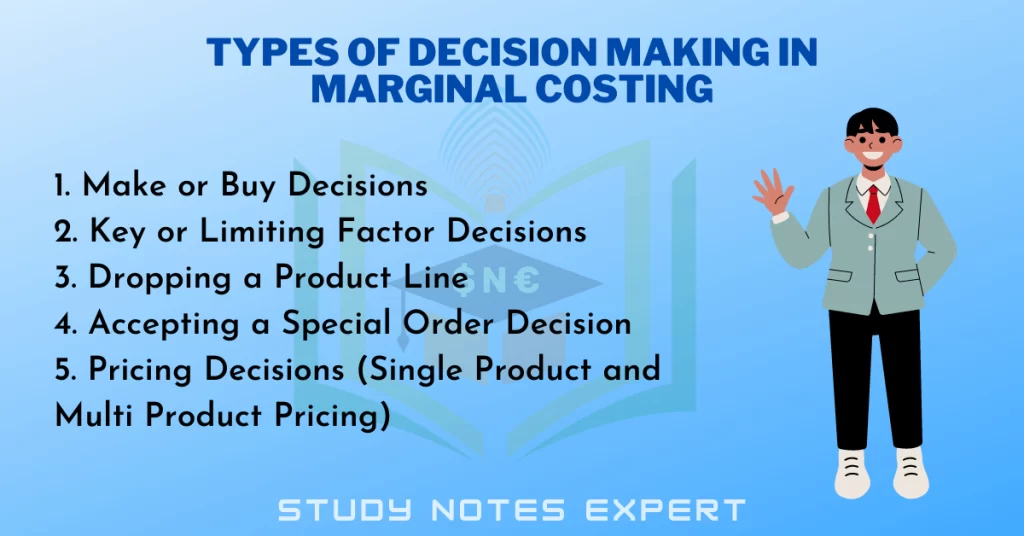

Multiple Types of Decision Making in Marginal Costing

1. Make or Buy Decisions

A firm may buy or manufacture components and spare parts. Marginal costing techniques may determine which action is more beneficial for the firm. For this purpose, the marginal cost of manufacturing is compared with the purchase price from the market. The firm may manufacture the product if its marginal cost exceeds the purchase price. It is one of the major decision making in marginal costing. Other factors, such as capacity utilization, should also be considered while making such a decision. In the case of unused capacity, only variable costs should be compared with the market price, while if the firm is working at total capacity, the opportunity costs should also be considered.

Factors Influencing Make or Buy Decision

The following make or buy decision factors should be kept in mind:

i) Plant Capacity

Subcontracting is generally advisable when the business is expanding, or the sales are seasonal.

ii) Profit Maximisation

The firm may decide to outsource the production of less profitable products.

iii) Specialisation

The products requiring specialized techniques may be better bought from outside.

iv) Nature of Product

The products should be manufactured internally if their consistent supply is required.

v) Secrecy

It is better to manufacture the parts if the firm wants to maintain its trade secrets.

2. Key or Limiting Factor Decisions

A key factor may be defined as “a factor which may limit the production or profit of a firm.” Sale is the most common limiting factor. The firm’s production is generally limited by its capacity to sell. Other limiting factors may be materials, labor, capital, or plant capacity. In such cases, the management may need to decide which products to produce and which quantity.

Without any limiting factor, the firm will decide its production strategy based on the P/V ratio. However, if there are limiting factors, the decision is made using contribution per unit of limiting factor. In the presence of a limiting factor, the profit may be maximized by making a contribution analysis for that factor.

3. Dropping a Product Line

A firm may redesign its product mix by “adding” or “dropping” a product. The firm may also stretch its product line up or down. Stretching up involves using better technology while stretching down involves the inverse. These decisions may be undertaken in response to structural changes in the market. It is one of the important decision making in marginal costing.

In a multi-product environment, the managerial decision to add a new product may lead to higher sales and associated costs, while dropping a product may cause inverse. Management may compare the differential costs and incremental revenue for such decisions.

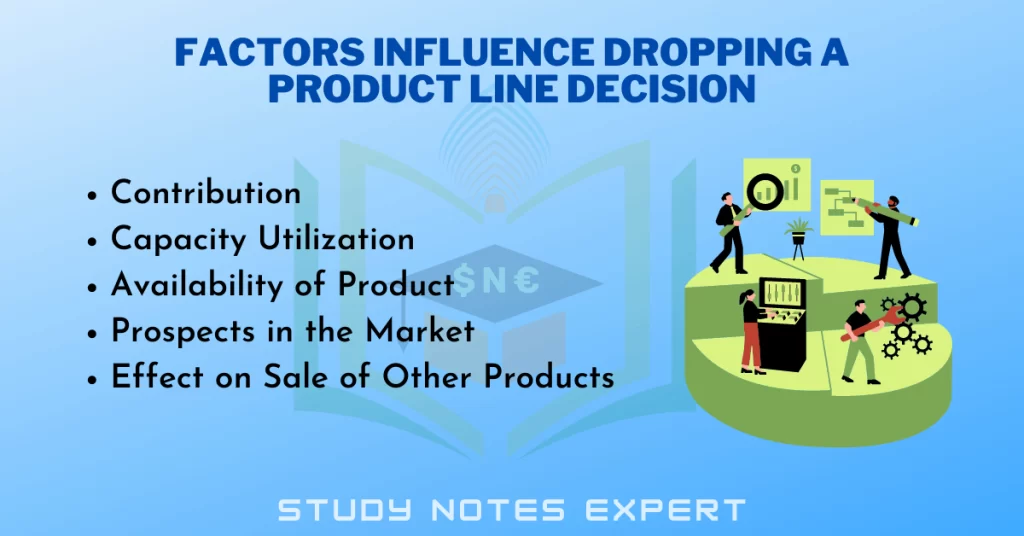

Factors Influence Dropping a Product Line Decision

The following factors should be considered before deciding on dropping a product line:

i) Contribution

The contribution given by the product is different from the profit. Profit is arrived at after deducting fixed costs from contribution. Fixed costs are apportioned over different products on some reasonable basis which may need to be more correct. Hence, contribution gives a better idea about the profitability of a product as compared to profit.

ii) Capacity Utilization

The capacity utilization, i.e., whether the firm works to total or below standard capacity. If a firm has idle capacity, the production of any product which can contribute toward the recovery of fixed costs can be justified.

iii) Availability of Product

The availability of products to replace the product the firm wants to discontinue already accounts for a significant proportion of the total capacity.

iv) Prospects in the Market

The long-term prospects in the market for the product.

v) Effect on Sale of Other Products

In some cases, discontinuing one product may result in a sharp decline in sales of other products affecting the firm’s overall profitability.

4. Accepting a Special Order Decision

Sometimes a decision regarding accepting a particular order is to be made. This, however, depends on the availability of spare capacity. The contribution available from such an order helps in making such a decision.

5. Pricing Decisions (Single Product and Multi Product Pricing)

Determining the selling price is a critical managerial decision. Various factors, such as market conditions and regulations, also impact this decision. Following are the various circumstances under which management may have to take such decisions:

i) Pricing under normal conditions

ii) During the stiff competition

iii) During the trade depression

iv) For accepting special bulk orders

v) For accepting additional orders utilizing idle capacity

vi) For accepting foreign orders and exploring new markets

Fundamental Principles of Pricing Decisions

Decision-making is a continuous process in a company, and the managers make different decisions from which the most critical decisions are related to pricing. Listed below are some of the significant pricing decisions taken by the managers:

i) Price setting for an innovative or new product.

ii) Price determination under perfect competition of the products traded under private labels.

iii) Tackling with price strategy opted by the competitors in the market.

iv) Pricing bids in conditions of open and sealed biddings.

Conclusion

The concept of decision making in marginal costing plays a vital role in managerial decision-making procedures. Various decisions can be made through marginal costing strategies, which provide managers with treasured insights into their services or products’ value structure and profitability. The diverse decision-making in marginal costing provides managers with a scientific framework to investigate costs, revenues, and profitability. Managers could make knowledgeable choices that maximize the agency’s economic performance by considering the total fees and contribution margins.