A ratio may be Meaning be defined as an arithmetical definition expression of a ratio in which analysis shows the relationship of one number to another. In mathematical terms, a ratio is the quotient of two numbers.

According to Kohler, “A ratio is the relation, of the amount, a, to another, b, expressed as the ratio of a to b; a: b (a is to b); or as a simple fraction, integer, decimal fraction or percentage”. Ratio uses two numbers & is obtained by dividing one number by another. It expresses one number in terms of another.

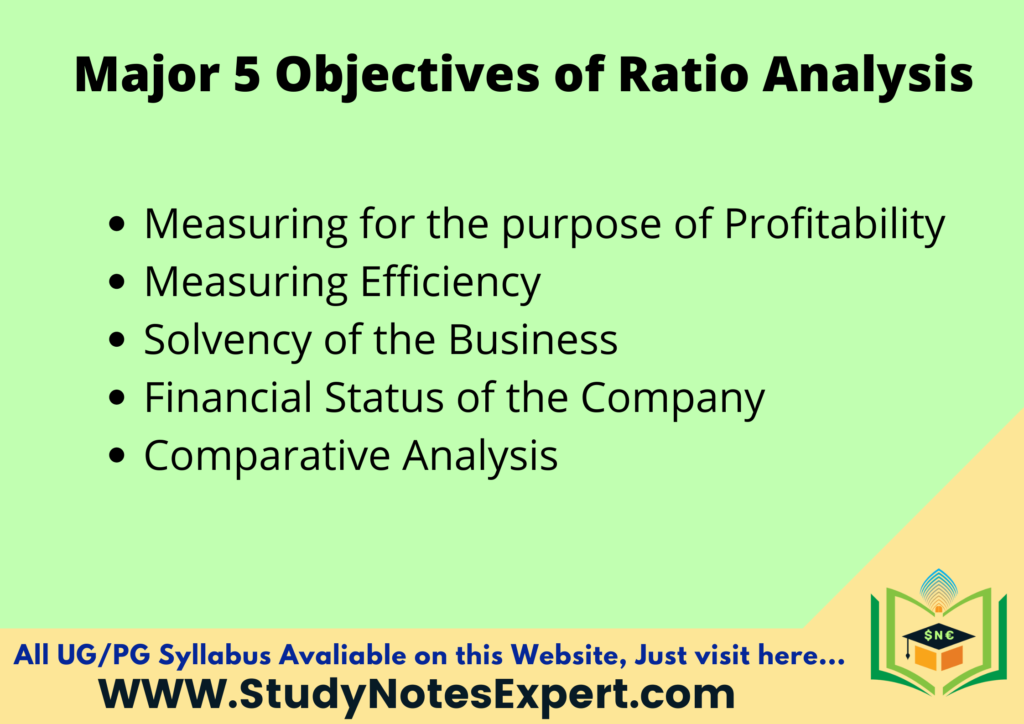

Major 5 Objectives of Ratio Analysis

There is some objective of the ratio analysis. All are very essential and we will mention them in the below section.

1. Measuring for the purpose of Profitability

It is used to measure profitability in Various ratios such as net profit, gross profit, and expense ratio.

2. Measuring Efficiency

Operating ratios are calculated for the purpose of measuring the operational efficiency of the business.

3. Solvency of the Business

Solvency ratios establish the relationship between the total assets and total liabilities of a concern. It helps to show whether the firm has enough assets to fulfill its debt obligations. Any firm which has enough assets will be considered solvent.

4. Financial Status of the Company

Fixed assets ratio and debt-equity ratio come under this category. These ratios are used to determine the financial status of the company. It is also useful for determining and comparing the long-term and short-term financial standing of the firm. For long-term financial status, various ratios such as proprietary ratios and fixed assets ratios are used. Current and Liquid ratios are used for determining short-term financial status.

5. Comparative Analysis

Ratios can be used for making temporal comparisons between the performances of the business. It can also be used for comparing two business identities having similar or different features. This analysis helps in determining the strengths and shortcomings of a business.

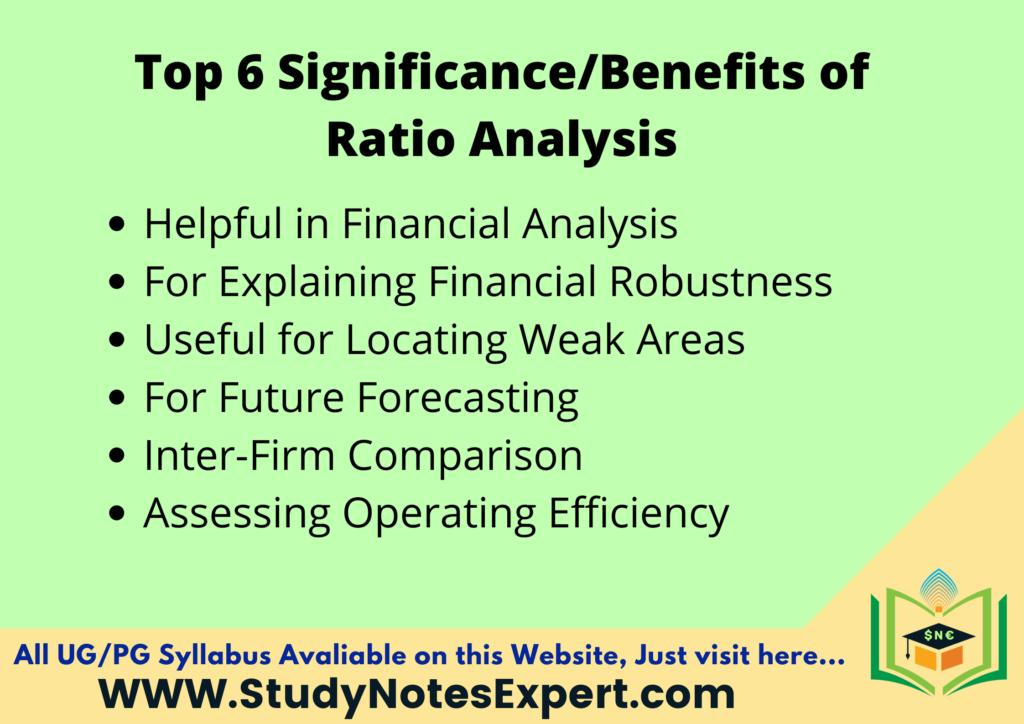

Top 6 Significance | Benefits of Ratio Analysis

There are some benefits of Ratio Analysis. All are very essential and we will mention them in the below section.

1. Helpful in Financial Analysis

Ratio analysis helps businesses in assessing their financial standing. It can be used for short-term as well as long-term financial analysis. Financial statements such as Profit & Loss Account and Balance Sheet are used for this purpose.

2. For Explaining Financial Robustness

Various ratios such as net profit ratio and debt-equity ratio may be used for expressing the financial health of the business.

3. Useful for Locating Weak Areas

Ratio analysis can be used for finding areas of weakness such as a high ratio of expenses or an increase in debt and taking remedial measures.

4. For Future Forecasting

Financial ratios can be used for the purpose of future planning and forecasting by the way of budgeting.

5. Inter-Firm Comparison

Financial analysis facilitates inter-firm comparison by bringing their performance to the same scale.

6. Assessing Operating Efficiency

Ratio analysis not only shows the financial standing of the business but also helps in evaluating operating efficiency

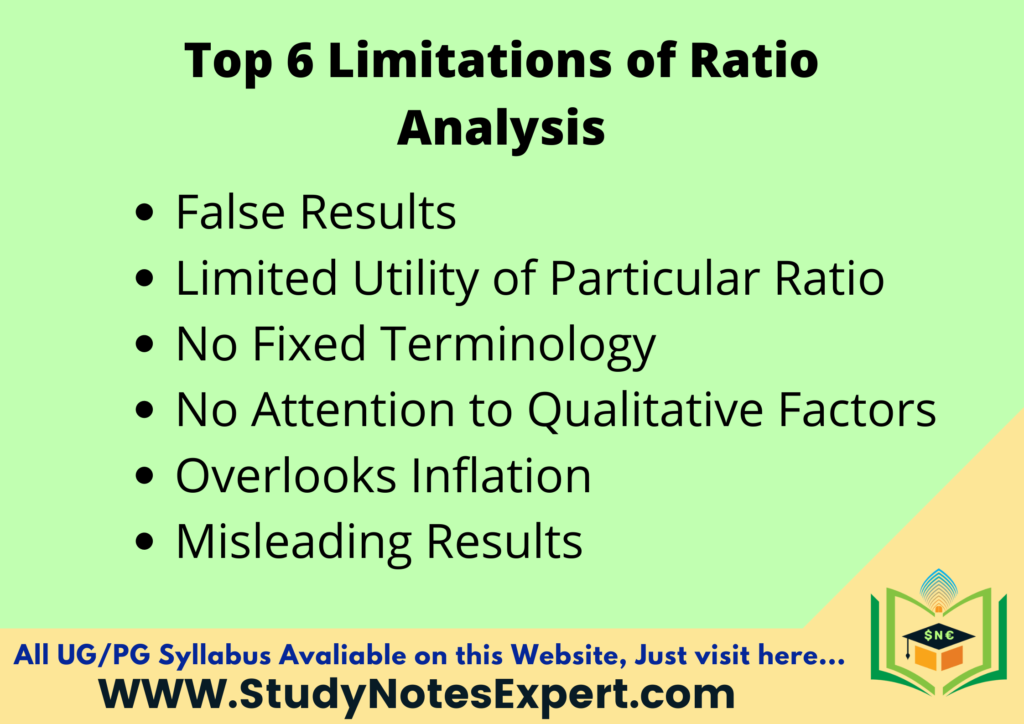

Top 6 Limitations of Ratio Analysis

There are some limitations of ratio analysis. All are very essential and we will mention them in the below section.

1. False Results

Ratio analysis is calculated using financial statements. The analysis would be incorrect if the statements are erroneous.

2. Limited Utility of Particular Ratio

In order to make a comprehensive analysis, it is important to use different ratios. A particular ratio may give misleading results. It is advisable to use various ratios for making meaningful and correct conclusions.

3. No Fixed Terminology

Ratio analysis is still evolving and various terms may be interpreted in different ways. This makes comparison difficult. For example, a ratio requiring the use of profit may be calculated using profit before tax or profit after tax. This may give erroneous results.

4. No Attention to Qualitative Factors

Ratio analysis is quantitative and does not take into account qualitative factors. This gives a one-sided view.

5. Overlooks Inflation

Since ratio analysis does not pay attention to changes in the price level, the temporal comparison does not serve many purposes.

6. Misleading Results

Ratio analysis brings financial statements of different firms to the same level. Such analysis does not provide information about the magnitude of their operations.

Major 4 Types of Ratio Analysis

We will discuss all types of ratio analysis. You can know this in the following section.

- Liquidity Ratio: These ratios are used to determine the short-term solvency of the firm. In other words, it analyses the firm’s ability to meet its current obligations. Liquid ratio, absolute liquid ratio, and current ratio are some of the ratios included in this category.

2. Solvency/Leverage Ratios: These ratios determine the extent to which an enterprise makes use of borrowed money. The main ratios included under this category are debt-equity ratio, proprietary/equity ratio, interest coverage ratio, and capital gearing ratio. These ratios help to determine a company’s long-term solvency.

3. Profitability Ratios: Gross profit ratio, net profit ratio, operating ratio, and expense ratio are some of the main examples of profitability ratios. These ratios calculate the overall performance of the business by using ratios such as return on equity, market capitalization ratio, and price-earnings ratio.

4. Activity/ Turnover Ratios: These ratios are calculated to assess a firm’s efficiency in employing its assets. These ratios are also known as turnover ratios as these ratios calculate the velocity with which assets are converted into sales. Several types of ratios included in this category are – fixed asset turnover ratio, debtor’s turnover ratio, and stock turnover ratio.

1) Liquidity Ratio

Liquidity is the ability of the business to meet its current liabilities this measures short terms robustness of the business. The ratio also assesses the liquidity of current assets held by the business. Current assets should be liquid or near liquid to meet short-term obligations.

i. Current Ratio

This ratio is also known as the ‘Working Capital Ratio’ and is used for determining the short-term financial position of the firm. It is done by matching the total current assets of the firm with its current liabilities.

Following is the formula used for calculating:

Current Ratio = Current Assets / Current Liabilities

ii. Quick or Acid Test or Liquid Ratio

This ratio is also known as the ‘Liquid or Acid Test Ratio’. The quick ratio is used to determine the short-term solvency of the firm. it describes the relationship between current liabilities and quick assets. The quick ratio measures the firm’s ability to meet its current obligations. This ratio is generally used in conjunction with the current ratio.

This ratio can be calculated as below:

Quick Ratio = Quick Assets / Current Liabilities

OR

Quick Ratio = Quick Assets / Quick Liabilities

Quick assets have the characteristic of easy conversion into cash and include cash, debtors, temporary investments, and bills receivable. It does not include inventory and prepaid expenses since these assets take considerable time and effort to convert into cash.

Quick Assets = Current Assets – (Stock + Prepaid Expenses)

2) Leverage/Solvency Ratio

This ratio analysis also deals with the long-term solvency position of the business as this helps to know whether the business would also be dealt ably with to honor interest payment and principal payment commitments.

i) Debt-Equity Ratio

This ratio is also known as the ‘External-Internal Equity Ratio’. This ratio is used to determine the efficacy of a firm’s long-term financial planning. This ratio shows the relationship between equity funding and debt funding.

Formula:-

Debt-Equity Ratio = Total Long-term Debt / Shareholders Funds

OR

Debt Equity Ratio = External Equities / Internal Equities

ii) Proprietary Ratio

This ratio establishes the relationship between proprietors’ funds and the total assets of the business. The main purpose of this ratio is to determine the sources for financing the assets.

i) Proprietors’ Funds

ii) Total Assets

Formula:- Proprietory Ratio =Proprietors Funds / Total Assets

iii) Interest Coverage Ratio/ Debt-Service Ratio

This ratio establishes a relationship between interest on long-term debt and net profits before interest and taxes. It is useful for determining the capability of a business in meeting its fixed interest obligations for its long-term loans.

Formula:- Interest Coverage Ratio = Net Profit before Interest and Taxes / Interest on Long-term Debt

3) Profitability Ratios

A business exists to make profits. It requires profits not only for survival but also for expansion and diversification. Profits can be used for determining the efficiency of management and employees. It is also useful for providing security to creditors.

i) Gross Profit Ratio

This ratio is known as the gross margin ratio for the trading margin ratio. This ratio is generally expressed in percentages and shows the relationship between the net sale and gross profit.

Gross profit Ratio = Gross profit / Net sales × 100

ii) Net Profit Ratio

This ratio is calculated by dividing net profit by net sales for the conversion period. Formula is –

Net Profit Ratio = Net Profit / Net Sales × 100

iii) Operating Ratio

This ratio measures the relationship between sales and the expenses incurred for making such sales and the formula is –

Operating Ratio = Cost of goods sold + Operating expenses / Net sales × 100

iv) Operating Profit Ratio

This ratio is a type of net profit ratio and determines the relationship between operating profit and sales the formula is-

Operating Profit Ratio = Operating Profit / Net Sales × 100

v) Expenses Ratio

This ratio shows the relationship between several expenses and net sales. This ratio depicts the increase and decrease of expenses.

Expense Ratio = Amount of Expenses / Net Sales × 100

vi) Earning per share

This ratio is calculated to find profitability per share and the formula is:

Earning per share = net profit after tax, interest, and preference dividend / Number of equity shares

vii) Market capitalization ratio

This Ratio established the relationship between earnings per share and market share and the formula is: Capitalization Ratio = Earning per share / Market price per share × 100

4) Activity / Turnover Ratio

This asset need to be managed efficiently for this purpose battery management assets help to generate higher profit for the business this activity ratio is also known as the turnover ratio.

i) Fixed Assets Turnover Ratio

The fixed asset turnover ratio matches fixed assets with sales revenue. This ratio shows the efficiency with which the business uses its fixed assets for the purpose of generating revenue and profit.

Fixed Assets Turnover Ratio = Net Sales / Net Fixed Assets

ii) Stock Turnover Ratio

This ratio is also known as the inventory turnover ratio or stock velocity ratio. It shows the relationship between the cost of goods sold and average inventory.

Stock Turnover Ratio = Cost of goods sold / Average Inventory

iii) Debtors Turnover Ratio

This ratio is also known as the Ratio of Net Sales to gross Receivable or Debtor’s Velocity. This ratio shows the relationship between the average amount receivable and net credit sales.

Debtors Turnover Ratio = Total Sales / Closing Debtors.

iv) Creditors Turnover Ratio

This ratio shows the relationship between net credit purchases and average trade creditors. This ratio is closely related to the concept of float.

Creditors Turnover Ratio = Total Purchases / Closing Creditors

v) Total Assets Turnover Ratio

This ratio is the relationship between sales and total assets this ratio is used to measure the overall activity and performance of the business concern.

Total Assets Turnover Ratio = Sales / Total Assets

What is meant by Ratio Analysis?

Ratio analysis analyses financial statements for a company. Analysts use them to determine a business’s profitability, liquidity, and solvency. Analysts use current and past financial accounts to assess a company’s performance. They utilize the data to determine if a company’s financial health is rising or falling and to compare it to competitors.

What are the 4 Types of Ratios?

There are 4 main types of ratio analysis.

1. Liquidity Ratios

2. Solvency Ratios

3. Profitability Ratios

4. Turnover Ratios

What are the Five Usefulness of Ratio Analysis?

The benefits of ratio analysis are as follows:

1. Ratio Analysis helps the competitors in Inter-firm comparison.

2. It helps in forecasting and planning the budget.

3. Ratio Analysis helps users provide information about the organization’s progress.

4. Also, estimating future events is done based on experience.

5. It helps in assessing operational efficiency.